I’m at the mall with my friends, and I see a pair of shoes that I absolutely love. “Everyone’s wearing them,” I think. “Shouldn’t I have a pair too?” Just as I decide to buy them, I suddenly realize I don’t have any cash. But then I remember–I can use my credit card!

Thousands of teens make decisions like this every day, swiping the plastic to buy whatever they want.

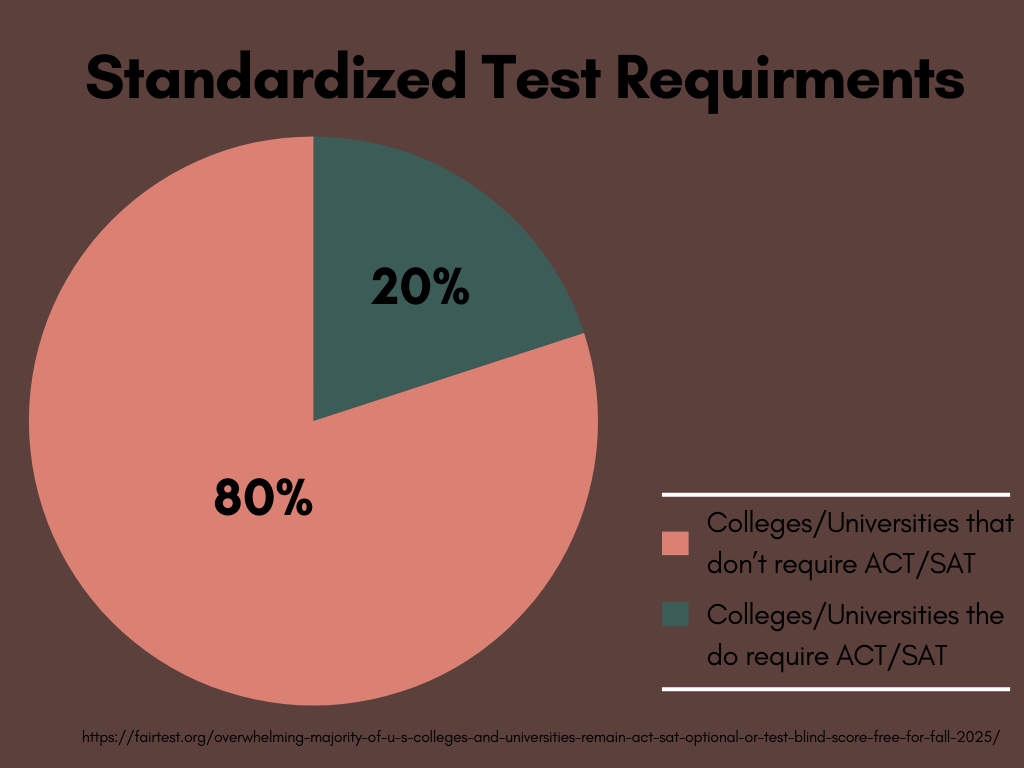

51 percent of teens believe credit cards are more convenient, according to research by AAA Fair Credit Foundation. Today 31.8 percent of high school seniors use a credit card. It’s much more convenient to carry that thin, plastic card than lumpy bills. You can buy anything, anytime, without needing enough cash on hand. And most of all, having a credit card makes you a real adult, right?

Well, sort of. Credit cards used in the right way have the potential to teach wise financial habits and credit card knowledge. However, without the correct knowledge, credit cards can teach poor financial habits and encourage reckless spending. They can have serious negative consequences that far outweigh the benefits of having the latest shoes.

There are three ways to have a credit card in high school. When a teen has a secured card, the debt is his responsibility. At the end of the month, if the student has not made the monthly payment on his loan, the bank will take it out of his savings account. On the other hand, on an authorized user card, the parents are responsible for the debt. A joint card splits the responsibility for the debt between the teen and his parents.

Each of these three options presents its own set of results. A secured card is the best of the three options, offering teens the opportunity to learn firsthand the monetary responsibility of having a credit card. Also, even if a teen is ignorant about the monthly payments on his loan, he’ll figure it out pretty quickly when the money from his savings account disappears.

“I have a Visa credit card under my name, and I have a checking and savings accounts through it,” senior Julie Targy said. “I love it. It’s easy and faster than money, since you can swipe it.”

Joint cards allow parents to have the most control over the teen’s spending, since they can set limits on the card amount. Being responsible for part of the debt can teach teens about financial responsibility, while the limit will put a curb on their spending.

“I want to think they [credit cards in high school] are irresponsible, because I want to think students are responsible for their money,” junior Daniela Cortes said. “But I’m pretty sure you can put a limit on it, and if you can that’s totally fine.”

An authorized user card definitely has the most destructive potential of the three options, taking all responsibility off teens’ shoulders. The extent of spending, and the amount of debt racked up, depends completely on the teen’s previous spending habits, whether good or bad. Unfortunately, this option is the easiest to get, so it’s the most often used.

“My parents pay for everything on my card. I definitely spend more money with my credit card than I would without it,” senior Lukas Link said.

So both secured and joint cards have potential to teach valuable lessons. However, in order to actually educate, credit cards need to be paired with financial knowledge.

Teens need to learn about personal finance, loans, debt and interest, and knowledge of the consequences of overspending. Simply giving teens credit cards won’t teach them these important lessons. Kids who only show up at sports practice or sit at a piano won’t become star athletes or gifted musicians. Only instruction in sports and music will nurture ability and knowledge. Similarly, monetary education is needed in order to really teach solid financial habits.

With the right supplements, like a personal finance class, limits on spending and an understanding of debt and interest, both secured and joint cards can teach important skills. Teens can gain both the knowledge and experience needed for successful financial habits. Combined with an understanding of money, they’ll be less likely to make impulsive buys, like those shoes that everyone has, just because they have a credit card.

However, if this knowledge isn’t there, credit cards can be a tool for disaster. People spend 47 percent more when they’re using a credit card, a fact that could rack up debt for teenagers. The authorized user card especially can wreak havoc on unsuspecting students’ monetary present and future.

Without the necessary information and education, credit cards in high school offer too many negative consequences. If all they will bring are debt and lessons in financial irresponsibility, then credit cards just aren’t worth it.

Julia Palomino

Reporter